Putting Clients First: The Accredited Investment Fiduciary® Difference

Some industry analyses estimate that only a small percentage of financial advisors in the U.S. operate under a fiduciary standard. This is important because fiduciaries are legally and ethically required to put their clients’ best interests first. Registered representatives operating under the suitability standard must ensure that recommendations are appropriate for clients, while fiduciary advisors are required to act in their clients’ best interests.

At SOUND Wealth Management Group, our approach is rooted in the fiduciary standard and reflects our commitment to transparency, objectivity, and care. Both Gary and Brandon have earned the Accredited Investment Fiduciary® (AIF®) designation, which demonstrates specialized training in applying fiduciary principles with consistency and diligence.

For our team, fiduciary responsibility is not simply a rule to follow; it represents our ethical foundation and the way we choose to serve our clients every day. Choosing a fiduciary advisor supports a transparent and objective approach that aligns with your values.

Key Highlights

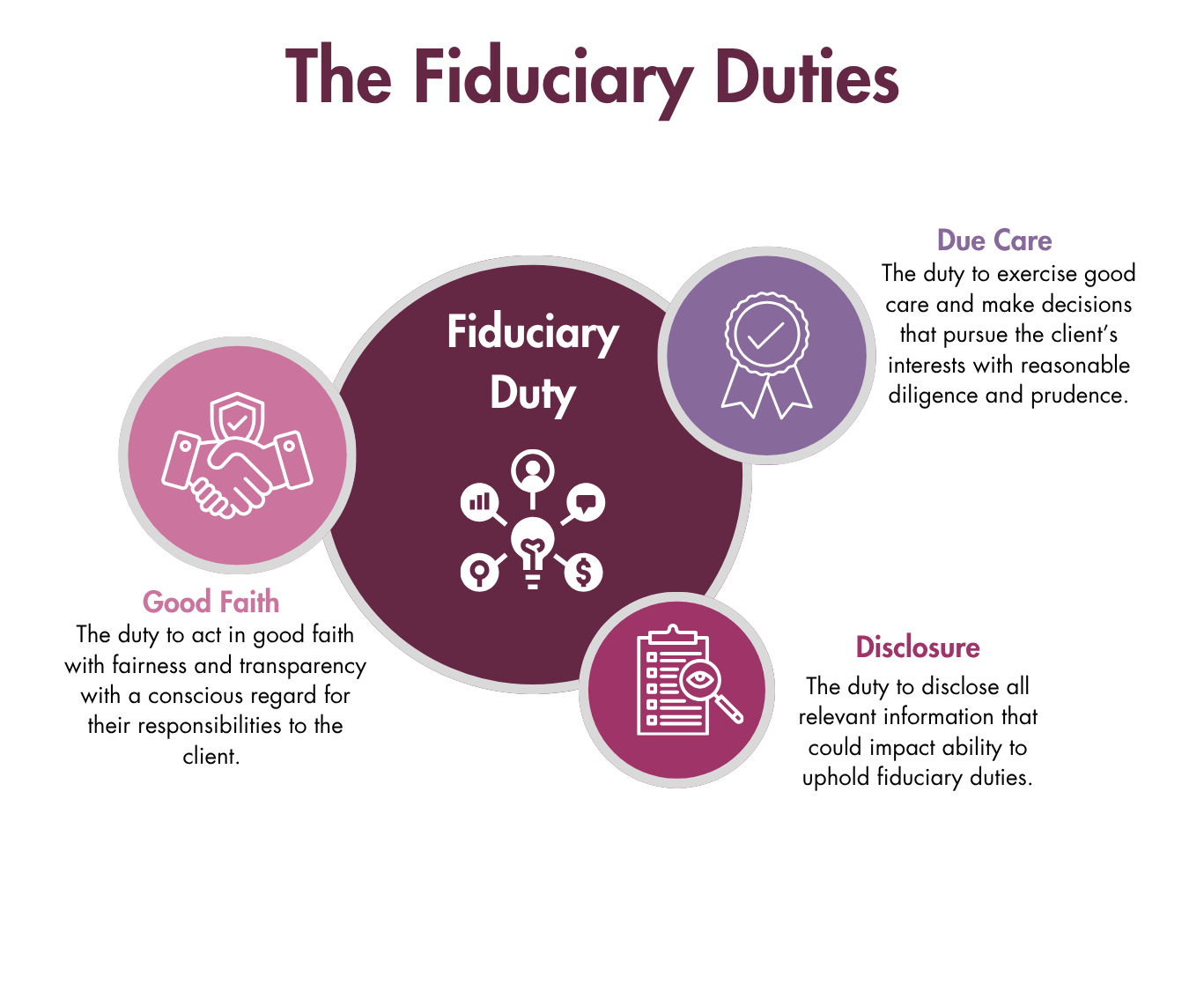

- Fiduciary duty requires advisors to put their clients’ interests first. It emphasizes transparency, ethical conduct, and accountability.

- Surveys show that most Americans believe financial professionals should act in their clients’ best interests.

- SOUND Wealth Management Group applies fiduciary principles through personalized financial planning and education for families, individuals, and businesses.

Defining Fiduciary Duty in Financial Advisory

Fiduciary duty is widely recognized as one of the most rigorous standards of care in financial services. It requires advisors to:

- Act in good faith and in the best interests of their clients.

- Disclose and manage potential conflicts of interest.

- Communicate fees and strategies with full transparency.

By adhering to this standard, fiduciary advisors promote trust and accountability, helping clients receive advice that is objective and aligned with their individual goals and circumstances. When investors work with fiduciary advisors, they benefit from a structured process that aims to reduce conflicts of interest and provide clear, documented strategies to help pursue financial security across areas such as retirement planning, debt management, investments, and legacy planning.

Disclosure Note:

The Accredited Investment Fiduciary® (AIF®) designation is issued by Fi360, a Broadridge company. It demonstrates specialized training in fiduciary responsibility and requires ongoing continuing education. FINRA and the SEC do not endorse any professional designations.

For a full description of Janney's investment advisory products and services, including investment programs managed by Janney Capital Management LLC, please refer to Janney's and Janney Capital Management's Form ADV Part 2 (i.e., Investment Management Disclosure Brochure), available on Janney's website or by contacting your Janney Financial Advisor.

For additional information or questions, please consult with your Financial Advisor or the Branch Office Manager. For more information about Janney, please see Janney's Relationship Summary (Form CRS) on www.janney.com/crs which details all material facts about the scope and terms of our relationship with you and any potential conflicts of interest.

SOURCE INFO:

Industry & Fiduciary Statistics

Investment Adviser Association — Industry Snapshots

https://investmentadviser.org/industry-snapshots

Human Investing — Only 4.92% of advisors are true fiduciaries. Is yours?

https://humaninvesting.com/450-journal/only-5-percent-of-advisors-are-true-fiduciaries

CFP Board — Survey: Americans Want Retirement Investment Advice to Be in Their Best Interest

Fiduciary vs. Suitability Standards

SmartAsset — Fiduciary vs. Financial Advisor

https://smartasset.com/financial-advisor/fiduciary-vs-financial-advisor

SEC — Commission Interpretation Regarding Standard of Conduct for Investment Advisers (IA-5248)

SEC.gov | Commission Interpretation Regarding Standard of Conduct for Investment Advisers

FINRA — Suitability Rule (Rule 2111) Overview

https://www.finra.org/rules-guidance/rulebooks/finra-rules/2111