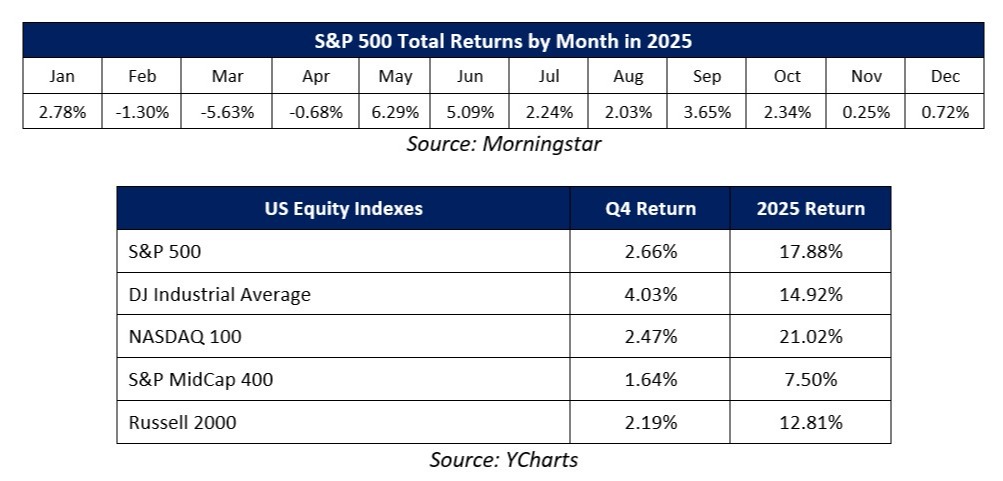

The S&P 500 rose to an all-time high in the fourth quarter as economic data showed solid growth, the Fed met investor expectations and cut interest rates and massive investment in AI infrastructure continued apace, supporting expectations for continued economic and corporate earnings growth in 2026. The S&P 500 logged a modestly positive return for the fourth quarter and an annual return of close to 20%, continuing a strong three-year run.

The S&P 500 started the quarter by hitting a new all-time high in early October, although volatility struck markets mid-month as trade tensions between China and the United States escalated once again. After several weeks of tit-for-tat trade restrictions and fee increases, in mid-October, President Trump threatened 100% tariffs on Chinese goods, dramatically escalating trade tensions between the two countries. That caused a short, sharp drop in U.S. stocks, although the volatility was ultimately short-lived thanks to a strong Q3 earnings season, rising expectations for a Fed rate cut and some de-escalatory rhetoric from President Trump about the U.S./China trade war. In the final days of October, those positive expectations were fulfilled as the Fed cut rates another 25 basis points and President Trump and Chinese President Xi met and struck another trade “deal” that de-escalated trade tensions and resulted in tariff reduction for Chinese imports to the U.S. The S&P 500 rose to another new all-time high in the final days of October and finished the month with a strong gain, rising 2.34%.

Volatility returned to markets in a more sustained way in November, thanks to rising doubts about future Fed rate cuts and disappointing AI-related news. Stocks dropped early in the month on further digestion of the recent Fed decision, which provided markets with a desired rate cut but also injected some doubt over whether the Fed would cut rates again in December. Then, in mid-November, several headlines and corporate updates cast some doubt about the expected return on investment of massive AI infrastructure spending. Additionally, not-as-good-as-hoped-for earnings by AI bellwether Nvidia further pressured tech stocks. Those two forces, fresh doubts about a December rate cut and mixed AI-related corporate news, led to a pullback of nearly 5% in the S&P 500 by mid-month. However, commentary by New York Fed President Williams helped stabilize markets around Thanksgiving, as Williams, who is seen as one of the most influential Fed members, implied he did expect the Fed to cut rates again in December. Williams’ comments sent expectations for a December rate cut surging and that, combined with the end of the longest government shutdown in U.S. history, helped stocks rally and close the month with a slight gain, rising 0.25%.

Volatility remained elevated in early December, however, thanks to the same forces that caused the November pullback (uncertainty over Fed policy and mixed AI news). Unlike November, though, none of the news was bad enough to cause a sustained pullback in stocks. Starting with the Fed, it cut interest rates a third time in 2025 at the December meeting but also signaled that it did not plan to cut rates again in early 2026. The mixed message wasn’t bad enough to disrupt markets, however, and with a new Fed chair looming in 2026, markets still believe more rate cuts are on the way. Turning to AI, corporate results remained mixed as underwhelming earnings reports by Oracle and Broadcom were offset by strong results from memory maker Micron. However, none of the news was bad enough to disrupt market momentum and with no more surprises lurking in 2025, year-end momentum carried the S&P 500 to new all-time highs late in the month.

In sum, 2025 was another strong year for markets, as continued investor enthusiasm for artificial intelligence, more Fed rate cuts and stable economic growth helped to offset decades-high tariff rates and general policy volatility.

Q4 and Full-Year 2025 Performance Review

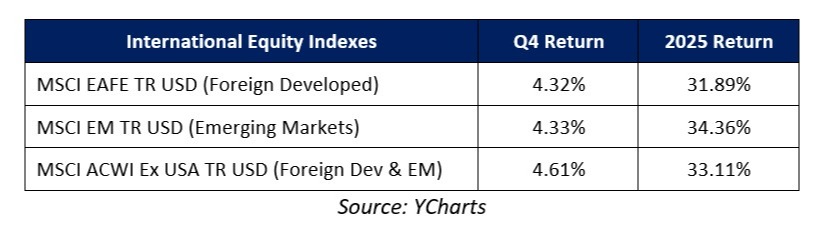

Continuing the strong year-to-date performance, all four major indices finished the fourth quarter with a solidly positive return. The Dow Industrials outperformed the other major averages thanks to strength in financials and industrials, as that index was not as impacted by mixed tech stock performance during the quarter. For the full year, however, the Nasdaq was the best performing major index as it benefitted from the large weightings to tech stocks, followed by the S&P 500 (where tech is the largest sector). The Dow Industrials and Russell 2000 both finished the year with solid gains, but they both underperformed the Nasdaq and S&P 500.

By market capitalization, large caps outperformed small caps in the fourth quarter and for the full year, thanks to strong gains in large-cap tech stocks, which were driven higher by AI enthusiasm and solid earnings growth. That said, small caps enjoyed solid returns for the fourth quarter and full year, due to falling interest rates and generally solid economic growth.

From an investment-style standpoint, value outperformed growth in the fourth quarter as mixed tech earnings weighed on growth funds, while solid economic data and more Fed rate cuts supported more cyclically oriented sectors that typically dominate value funds. For the full year, tech-heavy growth solidly outperformed value, however, as strength in AI stocks pushed growth styles higher on a full-year basis.

On a sector level, performance in the fourth quarter was mixed, as eight of the 11 S&P 500 sectors finished the fourth quarter with a positive return. However, for the second straight year, all 11 sectors ended the full year with gains. The healthcare sector was, by far, the best performer in the fourth quarter thanks generally to investors rotating towards more value-oriented sectors of the market, but also because fears that the prolonged government shutdown would lead to reduced federal healthcare spending went unfulfilled, and that boosted the outlook for healthcare stocks going forward. For the full year, technology and communication services sectors were the top performers, as both sectors benefitted from the substantial gains of AI-linked tech stocks.

Looking at sector laggards, utilities and real estate finished the fourth quarter with marginally negative returns. Utilities were pressured tangentially by a mild deterioration in sentiment towards the AI data center boom. Real estate, meanwhile, saw modest weakness thanks to lingering concerns about home affordability and after longer-dated Treasury yields rose to multi-month highs on concerns a “too dovish” Fed chair could reignite inflation in 2026. For the full year, consumer staples and real estate were the relative laggards, as generally speaking, investors preferred exposure to more AI and cyclical sectors given high AI enthusiasm and stable economic growth. More specifically, real estate faced year-long headwinds from higher interest rates while consumer staples stocks were negatively impacted by higher tariffs.

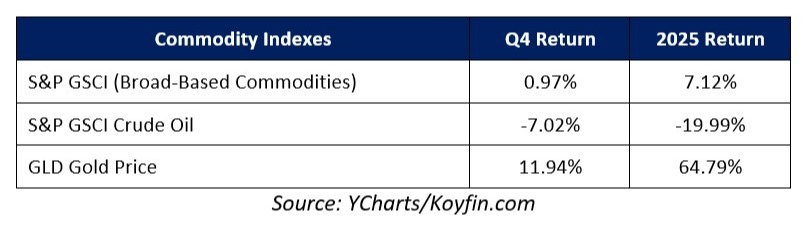

Foreign markets outperformed the S&P 500 in the fourth quarter and, for the first time since 2017, outperformed the S&P 500 for the full year. Foreign developed markets and emerging markets posted nearly identical returns in the fourth quarter thanks to solid economic growth in Europe and China and on expectations for rate cuts in the United Kingdom. For the full year, however, emerging markets slightly outperformed foreign developed markets thanks to falling global interest rates and a resilient Chinese economy.

Commodities saw mixed performance in the fourth quarter that largely mirrored the performance for 2025. Gold finished the fourth quarter and year with substantial gains. A weaker U.S. dollar, rising geopolitical tensions, stubbornly firm inflation and concerns about central bank independence all contributed to gold hitting a new all-time high in 2025 and turning in the best annual performance since 1979. Oil prices, meanwhile, declined sharply in the fourth quarter, which caused oil to post a negative annual return for 2025. Despite elevated geopolitical tensions, concerns about global oversupply of oil weighed on prices throughout 2025 and made it one of the few major assets to post a negative return for the year.

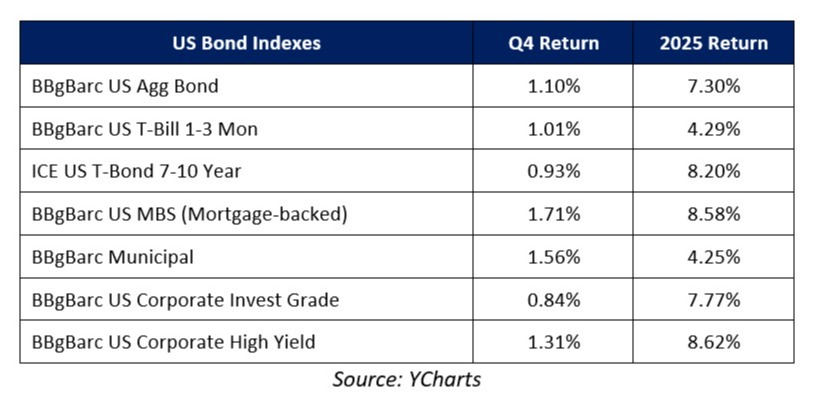

Switching to fixed income markets, the leading benchmark for bonds (Bloomberg Barclays US Aggregate Bond Index) realized a solidly positive return for the fourth quarter and that helped to round out a strong year of performance for the fixed income markets.

Looking deeper into fixed income, both long- and short-duration debt posted modestly positive returns in the fourth quarter, but longer-duration debt outperformed thanks to better-than-expected inflation readings and as concerns about the U.S. fiscal situation continued to recede. On a full-year basis, longer-duration bonds handily outperformed shorter-duration debt thanks to aforementioned declining concerns about U.S. fiscal ratios, solidly positive U.S. economic growth and still-robust foreign demand for longer-term U.S. debt.

Turning to the corporate bond market, high-yield bonds outperformed higher-quality but lower-yielding investment grade debt in the fourth quarter and for the full year as solid economic data and more Fed rate cuts prompted investors to reach for higher yield amidst a stable economy and expected earnings growth.

Q1 and 2026 Market Outlook

Markets begin the new year riding an impressive three-year winning streak that’s been powered by rate cuts, solid economic growth and extreme investor enthusiasm over artificial intelligence, and those positive factors remain in place as we begin 2026.

Starting with economic growth, despite major shifts in global trade policy and the longest government shutdown in U.S. history, the economy starts the new year on solid footing. Major economic metrics regarding consumer spending, service sector demand, business investment and employment are showing solid growth and that is important support for risks assets as we begin 2026.

On monetary policy, the Federal Reserve has cut rates aggressively over the past year and a half, easing the headwind on the U.S. economy. And despite some uncertainty about the number of future rate cuts in 2026, investors do still expect a generally “dovish” Fed as the Fed projections show another rate cut in the new year while a new Fed chair (likely to be appointed soon, and who will take office in May) is expected to push harder for more rate cuts and generally be more dovish than current Fed Chair Powell.

Finally, investor enthusiasm for the productivity and profit-boosting potential of artificial intelligence has been the main fuel behind this remarkable three-year bull market, and as we start 2026, AI enthusiasm remains broadly in place. In fact, major U.S. tech companies remain committed to spending hundreds of billions on AI infrastructure buildout and that should continue to power broader economic growth and strong tech sector earnings growth.

Bottom line, the factors that have fueled this three-year bull market remain in place as we start the new year and that means the outlook for markets and risk assets remains positive. However, that positive outlook should not be confused as being one without risks. And while the outlook is positive, it is also fair to say the market enters 2026 with weaker tailwinds than it’s had in the past few years.

Starting with economic growth, it’s true that most economic metrics are showing solid growth and there are few, if any, major economic metrics warning of an economic slowdown. However, the labor market has been losing momentum for most of 2025. The unemployment rate hit a four-year high late in 2025, and broadly speaking the labor market is in a current state of “No Hire/No Fire.” If layoffs start to increase in 2026, it will negatively shift the economic outlook and that would be a new, substantial headwind on stocks.

Turning to the Fed, while most expect the Fed to continue to cut rates in 2026, the reality is that the Federal Reserve is as divided as any of us have seen in a long time. Fed members appear torn over whether to continue to cut rates or hold them steady at current levels, and while the new Fed chairman is expected to be dovish, he is still only one vote on the committee. If the Fed more forcefully signals that rate cuts are over for the foreseeable future, that will be a negative surprise for markets.

Finally, enthusiasm for artificial intelligence stocks and the tech sector remains generally high, but skepticism about the massive amount of money being poured into AI infrastructure is rising and we saw that in mixed performance of tech stocks in the fourth quarter. If investor sentiment towards AI sours in 2026, that will remove a major tailwind from the tech sector and the entire market more broadly, and this is a risk that we will continue to closely monitor.

Perhaps one of the biggest surprises of 2025 was that continued geopolitical tensions and trade policy volatility did not negatively impact markets. But the reality is that both geopolitics and trade policy volatility are still potential negative influences on risk assets. An expansion of Russia’s war with Ukraine, a military confrontation between the U.S. and Venezuela, and the Supreme Court invalidating the 2025 tariffs are just some of the geopolitical and policy unknowns we must monitor in 2026, as each has the potential to cause surprise volatility.

Bottom line, while the outlook for markets is positive as we start the year, we won’t allow that to create a sense of complacency because, as the past several years have shown, markets and the economy don’t always perform according to Wall Street’s expectations.

As such, while we are prepared for the positive outcome currently expected by investors, we are also focused on managing both risk and return potential because, as last year once again demonstrated, a well-planned, long-term-focused and diversified financial plan can withstand virtually any market surprise and related bout of volatility.

At Towson Partners Wealth Management, we understand the risks facing both the markets and the economy, and we are committed to helping you effectively navigate this challenging investment environment. Successful investing is a marathon, not a sprint, and even intense volatility is unlikely to alter a diversified approach set up to meet your long-term investment goals.

Therefore, it’s critical for you to remain patient, and stick to the plan, as we’ve worked with you to establish a unique, personal allocation target based on your financial position, risk tolerance, and investment timeline.

Rest assured that our entire team will remain dedicated to helping you successfully navigate this market environment.

Please do not hesitate to contact us with any questions, or comments, or to schedule a portfolio review.

Sincerely,

Towson Partners