Major stock indices continued the 2025 rally and surged to new all-time highs in the third quarter as economic growth remained stable, tariff increases were no worse than feared and the Federal Reserve cut interest rates, beginning the long-awaited rate-cutting cycle.

Markets started the third quarter with a continuation of the year-to-date rally thanks, initially, to the passage of the One Big Beautiful Bill Act in early July. This legislation contained several pieces of economic stimulus including making the 2017 tax cuts permanent, reintroducing accelerated depreciation and committing billions to the development of domestic industries, providing the markets and the economy with a fresh dose of fiscal stimulus. But while that was the first positive market event in July, it was not the last. Second-quarter corporate earnings results (released in mid-July) were stronger than expected and importantly showed no significant signs that tariffs or policy uncertainty were weighing on results. Finally, in mid-to-late July, the Trump administration announced trade agreements with some of the largest U.S. trading partners including the EU, Japan and South Korea, while the U.S. and China agreed to extend their trade “truce” as the two sides negotiated toward a larger trade agreement. These trade “deals” reduced investor anxiety stemming from the re-imposition of reciprocal tariffs in early August and lowered trade-related concerns among investors. These factors, along with stable economic and inflation readings, helped to push the S&P 500 steadily higher and the index rose 2.24% in July.

The beginning of August brought an economic surprise, however, that temporarily paused the rally in stocks. The July jobs report, released on August 1st, was much weaker than expected, not just because job growth in July disappointed but also because there were substantial negative revisions to the May and June reports. The underwhelming employment data introduced the idea that the labor market was weaker than expected and that did slightly increase economic slowdown risks. However, the soft employment data also boosted expectations for a Fed rate cut, and at the Jackson Hole Economic Symposium Fed Chair Powell strongly hinted that a rate cut was coming at the September Fed meeting. Rising rate cut hopes helped to offset the underwhelming employment data and stocks ultimately continued their advance, as the S&P 500 rose 2.03% in August.

The rally accelerated in September despite growing signs that the labor market is indeed seeing some deterioration. The August jobs report was another underwhelming print showing just 22,000 jobs added that month, well below the consensus estimate. But like in August, the expectation for Fed rate cuts helped offset that negative employment report and the Fed did cut interest rates at the September meeting. Equally as importantly, Fed members signaled they expected two more rate cuts this year via the “dot plot.” The start of a Fed rate-cutting cycle, which should support the economy, combined with strong AI-related tech stock earnings from Oracle and Broadcom to send stocks higher and major U.S. stock indices all hit new all-time highs following that Fed rate cut, capping a moderate increase in September.

In sum, the third quarter was resoundingly positive for the U.S. economy and markets as economic data showed solid growth, inflation readings stayed mostly stable, the Fed cut interest rates, the U.S. reached trade agreements with major trading partners and AI-linked tech companies continued to produce better-than-expected earnings. Given these positives, major U.S. stock indices rallied solidly in the third quarter, just as they should have given this news.

Third Quarter Performance Review

Rising expectations for a rate cut; strong AI-related corporate results, and stable economic growth helped propel the major stock averages solidly higher in the third quarter.

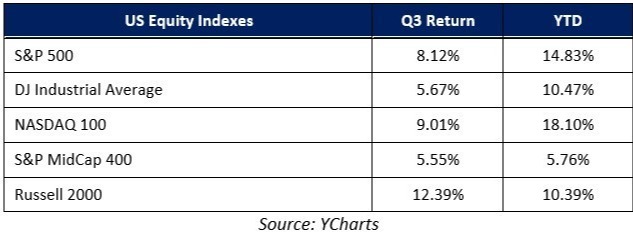

Starting with market capitalization, small caps outperformed large caps for the first time in 2025 as investors rotated out of large-cap stocks and into more economically sensitive small caps, as they historically have received the most benefit from lower borrowing costs that come with falling interest rates.

From an investment style standpoint, both growth and value ETFs were solidly higher in Q3 but growth outperformed value thanks to continued strength in AI-linked tech stocks, continuing a trend from the second quarter.

On a sector level, 10 of the 11 S&P 500 sectors finished the third quarter with a positive return. Tech and tech-aligned sectors (consumer discretionary and communications services) comfortably outperformed other market sectors and posted strong quarterly returns. Positive earnings results from AI-linked tech stocks such as Microsoft, Alphabet, Amazon, Nvidia, Oracle, Broadcom and others kept investor enthusiasm for AI-related investments high and that powered tech and communications services higher. The consumer discretionary sector, meanwhile, benefited from solid economic growth and expected lower interest rates, which should support consumer spending.

Looking at sector laggards, consumer staples was the only sector that finished the third quarter with a negative return. Investor preference for more economically sensitive sectors (given falling interest rates) and tariff related concerns pressured that sector, which finished the third quarter with a modest loss.

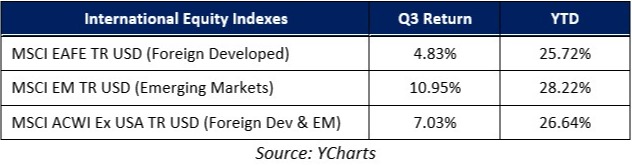

Internationally, foreign markets saw mixed performance vs. the S&P 500 as emerging markets outpaced U.S. stocks in the third quarter while foreign developed markets posted a positive return but relatively underperformed the S&P 500. Emerging markets handily outperformed the S&P 500 in Q3 thanks primarily to a weaker dollar, falling interest rates and a rebound in Chinese economic growth. Foreign developed markets also rallied in the third quarter but lagged the S&P 500, due in part to concerns about fiscal stress and slow growth in the United Kingdom.

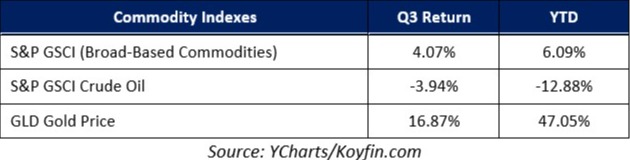

Commodities were solidly higher in aggregate in the third quarter but that result somewhat masked mixed internal performance. Gold surged to fresh all-time highs in the third quarter thanks to elevated inflation and the weaker U.S. dollar. Oil, however, declined as increased production from OPEC+ and concerns about global economic growth weighed on oil prices, especially late in the third quarter.

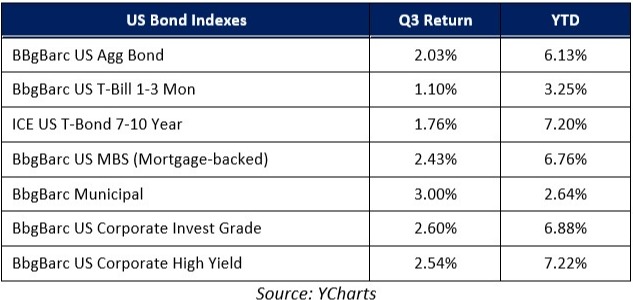

Switching to fixed income markets, the leading benchmark for bonds (Bloomberg Barclays US Aggregate Bond Index) saw a strong quarterly return despite elevated inflation readings, as expectations for rate cuts and labor market deterioration boosted demand for both short- and longer-term debt.

Looking deeper into the bond markets, longer-duration bonds comfortably outperformed those with shorter durations as investors reached for longer-term yield amidst underwhelming labor market data. Shorter-duration bonds also saw a positive return, however, as investors anticipated the start of a rate-cutting cycle by the Fed.

Turning to the corporate bond market, both investment grade bonds and lower-quality, high-yield bonds saw strong gains in the third quarter. Investment grade bonds slightly outperformed high yield bonds as the weakening labor market and slight uptick in economic concerns boosted the attractiveness of higher credit quality corporate bonds.

Fourth Quarter Market Outlook

Markets begin the final quarter of 2025 in a decidedly positive macroeconomic environment as the Fed is cutting interest rates, tariffs have not disrupted the U.S. economy (so far), broader economic growth remains stable and investment enthusiasm for AI-linked tech stocks remains high. Those factors propelled stocks steadily higher throughout the third quarter, added to already-solid year-to-date gains for major U.S. stock indices and boosted investor enthusiasm.

However, while the current macroeconomic setup is positive, it should not be confused with a riskless environment and continued gains in stocks are not inevitable. And as always, there are risks to the markets and economy we must monitor.

First, the labor market is deteriorating and that is an economic risk that needs to be monitored closely. Numerous employment indicators, in addition to the monthly jobs report, are signaling a loss of momentum. For now, they are not at levels that would increase concerns about overall U.S. economic growth, but if we see the unemployment rate continue to rise, investors will become more concerned about the state of the U.S. economy and that could be an unexpected negative influence on the markets, as an economic slowdown is not currently anticipated by investors or analysts.

Additionally, inflation remains stubbornly high. Headline CPI remains just under 3.0%, solidly above the Fed’s 2.0% target. Meanwhile, tariffs are now starting to impact broader parts of the U.S. economy and while analysts generally believe tariffs will produce only a one-time price increase and not create broader inflation, that outcome remains uncertain. Bottom line, there is a chance that tariffs further boost inflation in the fourth quarter and that could result in the Fed having to reconsider future rate cuts, which would produce a negative surprise.

Staying on tariffs, there remains substantial policy uncertainty with regard to trade and tariff policy. The Supreme Court will hear arguments on most reciprocal tariffs in November and if the Supreme Court upholds the lower court ruling invalidating tariffs, it could cause market volatility. While the removal of tariffs may initially boost stocks, it will also extend broader policy uncertainty, as the administration will likely try to reimpose tariffs using different legislation. Bottom line, markets embrace clarity and the longer trade policy uncertainty exists, the greater the chance that it becomes a headwind on growth.

Finally, AI and tech enthusiasm has driven the valuation of the S&P 500 to a historically high level. While elevated valuation, by itself, isn’t a negative influence on stocks, the high valuation does underscore this reality: A lot of profit growth is priced into the largest tech stocks and if AI-related capital expenditures from major tech firms begin to decline or AI adoption disappoints investor expectations, it could be a substantial surprise negative for markets.

In sum, the macroeconomic environment is currently positive as the economy and markets are benefiting from rate cuts, fiscal stimulus (via the One Big Beautiful Bill Act) and continued investor enthusiasm for AI-linked tech stocks. But we also recognize that risks remain on the periphery of both the markets and the economy.

At Towson Partners Wealth Management, we understand the risks facing both the markets and the economy, and we are committed to helping you effectively navigate this challenging investment environment. Successful investing is a marathon, not a sprint, and even intense volatility is unlikely to alter a diversified approach set up to meet your long-term investment goals.

Therefore, it’s critical for you to remain patient, and stick to the plan, as we’ve worked with you to establish a unique, personal allocation target based on your financial position, risk tolerance, and investment timeline.

Rest assured that our entire team will remain dedicated to helping you successfully navigate this market environment.

Please do not hesitate to contact us with any questions, or comments, or to schedule a portfolio review.

Sincerely,

Towson Partners