Market volatility spiked in the first quarter of 2026 as a surge in geopolitical tensions combined with stress in private credit markets and growing concerns that AI may pose threats to certain industries to push the S&P 500 moderately lower to start the year.

Geopolitical surprises started immediately in 2026 as on January 3, the U.S. military performed a daring raid in Venezuela and arrested Venezuelan President Maduro, causing a temporary pop in market volatility given uncertainty around the country’s vast oil supplies. The action proved limited, however, and the new Venezuelan leader pledged to work with the U.S., easing market tensions. Shortly after markets recovered from that initial surprise, we received another one, as the U.S. Attorney for the District of Columbia issued two grand jury subpoenas to Fed Chair Powell surrounding the renovation of the Federal Reserve building. That action renewed concerns about attacks on Fed independence, which, if compromised, could lead to sustainably higher inflation. In response, several prominent Republican Senators pushed back against the subpoenas and voiced support for Fed independence, easing market concerns. While these surprise headlines caused short bursts of market volatility, stable economic data and a generally solid fourth-quarter earnings season helped keep economic and earnings growth forecasts intact, while the Fed reminded investors at the January meeting that it still planned to cut rates again this year. Despite the headline volatility, the S&P 500 ended the month with a solid gain.

Volatility continued in early February, but this time it was more focused on specific sectors of the market such as tech and financials. AI company Anthropic released a Claude Cowork app that caused a steep decline in the software sector, as fears surged that AI advancements could ultimately eliminate the need for entire sectors of the economy. That idea jolted investors’ previous opinions that AI was nearly all beneficial to the markets and economy. Meanwhile, underlying fears of credit risks in private credit funds grew, as numerous large alternative asset managers limited redemptions from specific funds, fueling concerns there was a bubble in the industry. Finally, on the last day of February, geopolitical risks surged as the U.S. launched a massive attack on Iran, sparking a war between the two countries that effectively closed the Strait of Hormuz and drastically reduced available global oil supplies, which caused oil prices to surge overnight. These factors combined to push the S&P 500 slightly lower for the month but the index remained positive for the year.

The market declines accelerated in March as hopes for a quick resolution to the U.S./Iran war faded. While the U.S. and Israel dominated the conventional military conflict, Iran and its proxies attacked neighboring Gulf states’ energy infrastructure and oil tankers in the Persian Gulf, causing the price of oil to surge above $100/bbl and increasing pressure on the global economy. The S&P 500 fell modestly on the surge in geopolitical risks, although hopes of a ceasefire late in March did help limit losses. The S&P 500 declined moderately in March and finished the quarter in solidly negative territory.

The first quarter of 2026 saw volatility surge, as military conflicts combined with more traditional market concerns of overvalued assets (in private credit) and potentially negative impacts of AI to pressure stocks moderately, although still-stable economic growth and corporate earnings helped to support markets throughout the quarter.

First Quarter Performance Review

Market internals and performance in the first quarter were driven primarily by the U.S./Iran war, but also by concerns about private credit and potentially negative impacts from AI.

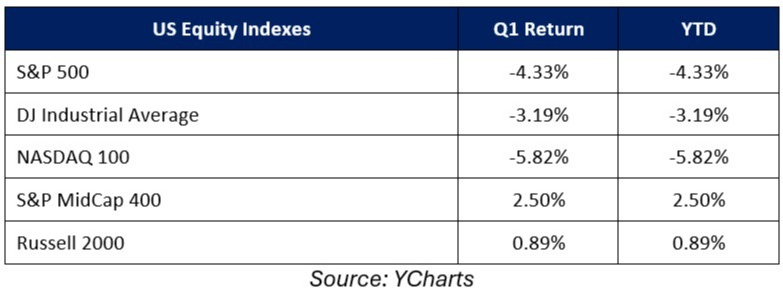

On an index level, the three major large cap stock indices finished the quarter with losses. The Nasdaq was the worst performer among them thanks to weakness in AI-related tech and software stocks. Small caps, however, relatively outperformed large caps as the Russell 2000 finished the first quarter with a small gain, as small-cap stocks are generally viewed as more insulated from the headwinds of the first quarter (i.e., geopolitical tensions, private credit worries, AI concerns).

Turning to value vs. growth, value massively outperformed growth in the first quarter and managed a modest gain, as value-focused strategies benefited initially from a rotation away from tech and towards sectors less exposed to AI. Additionally, late in the quarter, value styles benefited from the surge in the lower-multiple energy and materials sectors, which rallied following the outbreak of the U.S./Iran war. Tech-heavy growth strategies finished solidly lower for the quarter.

On a sector level, performance was mixed as six of the 11 S&P 500 sectors finished the quarter with a positive return. The best-performing sector in Q1, by a large margin, was energy, which surged more than 30% in the first quarter thanks to rising oil prices. The materials sector, which includes companies with heavy commodity exposure, also was a solid performer on rising natural resource prices following the U.S./Iran war. Finally, consumer staples and utilities also finished the first quarter with strong gains, as investors rotated to less volatile, more defensive parts of the market.

Looking at sector laggards, the financial sector was the worst-performing S&P 500 sector in Q1 and suffered solid losses, thanks to aforementioned private credit concerns. The consumer discretionary sector also posted a moderately negative return on worries that higher oil prices would reduce consumer spending. Finally, the technology sector dropped on weakness in software stocks and AI-linked technology stocks.

Internationally, foreign markets relatively outperformed the S&P 500 and ended the quarter with only a small decline, despite the surge in geopolitical risks. Emerging markets outperformed both developed markets and the S&P 500 and registered only a fractional loss despite the strong dollar, as the surge in commodity prices was seen as offsetting the rising U.S. dollar. Foreign developed markets declined in Q1, but only modestly, and solidly outperformed U.S. markets thanks mostly to the smaller weighting of tech shares in foreign indices.

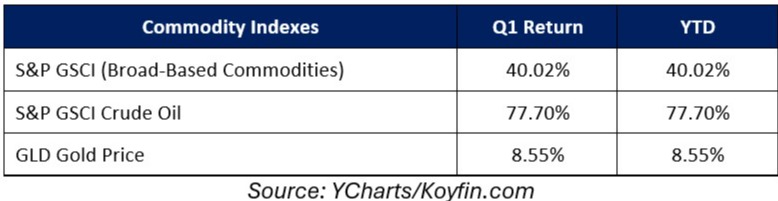

Commodities were generally speaking, sharply higher in the first quarter thanks to the surge in the geopolitical risk premium following the outbreak of the U.S./Iran war. Oil prices hit the highest levels since 2022 thanks to the U.S./Iran war and following Iranian attacks on Gulf oil infrastructure, which further reduced global supply. Gold, meanwhile, hit a new all-time high above $5,000/oz. early in the quarter but finished with just a moderate quarterly gain, as the surging dollar pressured gold prices late in Q1.

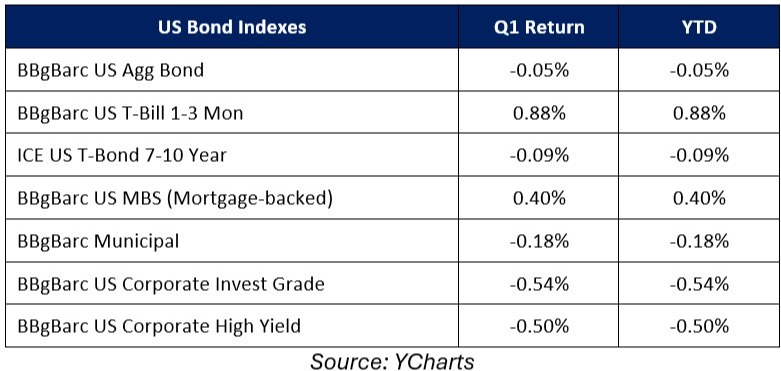

Switching to fixed income markets, the leading benchmark for bonds (Bloomberg Barclays US Aggregate Bond Index) finished the quarter with a slight loss as bonds were solidly higher mid-quarter but declined in March on rising inflation concerns, as surging oil prices and hotter-than-expected inflation readings reduced expectations for Fed rate cuts. Short-term bills modestly outperformed longer-duration bonds and logged a positive return as they are less sensitive to rising inflation risks compared to longer-duration debt.

Turning to the corporate bond market, both high yield and investment grade corporate bonds declined slightly in the first quarter as the U.S./Iran war and spiking oil prices raised concerns about an economic slowdown. Reflecting general investor anxiety about economic growth given the war and rising oil prices, both lower yielding but higher quality investment grade corporate bonds and high yield bonds (which have a better yield but also more credit risk) experienced similar small losses for the quarter.

Second Quarter Market Outlook

Stocks begin the second quarter facing three distinct market headwinds: Higher oil prices (a result of the U.S./Iran war), credit concerns (emanating from private credit funds) and worries that AI, while a transformative technology, could have unanticipated negative impacts on important market sectors. Each of these concerns will need to be resolved if the market is going to fully rebound from the Q1 declines, although it’s important to note that economic growth and corporate performance remained solid in Q1 and that is helping to support markets.

Starting with geopolitics, the focus for markets remains on the price of oil. Elevated oil prices pose a risk for the markets and economy in multiple ways including 1) No Fed rate cuts as the Fed worries higher oil prices may spur inflation, 2) Depressed consumer spending as higher gas prices reduce disposable income and 3) Tighter corporate margins given increased transportation and infrastructure costs. Ultimately, that could lead to stagflation in the economy, which would be negative for most assets. For geopolitical risks to fully recede, we will need to see a credible ceasefire agreement between all parties (the U.S., Israel and Iran), transit through the Strait of Hormuz return to something close to pre-war levels and a decline in oil prices back towards pre-war levels.

Private credit, meanwhile, is evoking memories of the financial crisis amongst more tenured investors, fueling fears that the recent influx of investor capital into private credit funds led to poor investing standards and overvaluation. While analogies to the financial crisis are understandable, it’s important to realize the private credit market is much, much smaller than the markets that caused the financial crisis and Fed officials have recently said they see no indication of a systemic problem. While that is reassuring, private credit concerns are still weighing on the financial sector, which is the second-largest sector in the S&P 500 by weight and an important market leader. An easing of private credit concerns and a rebound in the financials is needed to help the market further stabilize in the second quarter.

Finally, turning to AI, opinions on the impact of AI on the economy and markets have shifted from mostly positive to that of increased skepticism, and there are two main concerns associated with AI currently. First, that massive spending on AI infrastructure by large tech companies may ultimately have a poor ROI and depress future earnings. Second, that AI advancements may disrupt entire portions of the economy (such as the software sector) and lead to large job losses that hurt overall economic growth. Both of these concerns need to be addressed and countered for AI and the tech sector to fully rebound in Q2.

Bottom line, the first quarter did contain several negative surprises for investors and we begin the second quarter with uncertainty over geopolitics, credit and AI. But there are also positive factors at work that must be considered, including a still-resilient economy, strong corporate earnings growth and a Federal Reserve that is still signaling rate cuts. Those factors supported stocks and bonds in the first quarter and despite the volatility and elevated uncertainty, the outlook for the economy and markets is not universally negative and as we saw firsthand in Q1, the geopolitical and corporate landscape can change quickly.

At Towson Partners Wealth Management, we have experienced these types of markets before and are committed to helping you effectively navigate this challenging investment environment. Successful investing is a marathon, not a sprint, and through both bull and bear markets, we will remain focused on the diversified approach we have set up to meet your long-term investment goals.

Therefore, it’s critical for you to stay invested, remain patient, and stick to the plan, as we’ve worked with you to establish a unique, personal allocation target based on your financial position, risk tolerance, and investment timeline.

We remain vigilant towards risks to portfolios and the economy, and we thank you for your ongoing confidence and trust. Please rest assured that our entire team will remain dedicated to helping you successfully navigate this market environment.

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio review.