Surrounding you with a fortress of financial resources is how we help you retire and worry less about it. This fortress is made up of the 5 Pillars of Financial Planning. As you probably know from your own experience, success comes from having a plan, and that is exactly what we focus on. We take your input and create a customized plan, help you work that plan while managing your assets through the ups and downs of the market.

PILLAR 1: RETIREMENT PLANNING

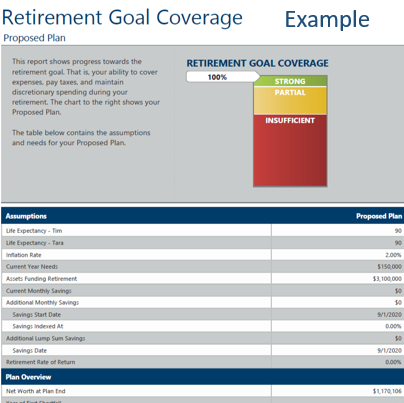

A crucial first pillar, this is an interactive and educational process of determining retirement goals and priorities and every single client goes through it with us. In short, it’s a process for determining when you can retire and how much monthly income you can retire on.

Through our “Discovery Meeting,” conversation and financial planning questionnaire, we are able gather the information that is instrumental in helping us develop a retirement plan that lasts throughout your lifetime. Additional information includes:

- Estimate of how much after-tax income you will need during retirement – we recommend starting with your current take home income. If you know you will no longer have a mortgage payment or you may have a car payment at retirement, you can adjust this amount up or down depending on your situation.

- Determine the sources for that income – we recommend going through statements for all those sources for example Social Security, pensions, IRAs, 401(k)s, deferred compensation, executive compensation, restricted stock, stock options, other tax-deferred accounts as well as annuities and joint investment accounts.

- Estimate a reasonable withdrawal based on the income you want and the sources of income you have – we utilize the most comprehensive financial planning solutions on the market called NaviPlan® to create various scenarios if needed to help with this

After creating your plan using NaviPlan®, we meet again and walk you through each year from now until you retire showing how your yearly contributions may affect your savings for retirement. Once you retire and contributions cease and withdrawals begin, you can see an estimate of what your income may look like each year from all your sources (social security, pensions, IRAs and after-tax accounts). We believe in the 4% Rule because based on historic returns, withdrawals may be safe for a thirty-year window. This becomes an even bigger part of the conversation because our focus is to protect assets once distributions begin because at that point, a big loss could permanently damage a portfolio. We also recommend updating the financial plan if your situation changes (change of employment, divorce, death of spouse, etc…) and again within a couple years before retirement.

PILLAR 2: INVESTMENT STRATEGY

We know you want to make the smartest decision with the wealth you’ve accumulated throughout your life. Before you know it you’ll be entering a different phase in life, the distribution or retirement phase, and we want to put your mind at ease about how long your money will last throughout retirement. If you hear yourself asking, “what is the best way to invest my money?” then we would love to help you.

Allocation by risk is the foundation of our investment process. To break that down, asset allocation means dividing your money into different buckets or asset classes (opposite of putting all your eggs into one bucket) to diversify. These buckets or asset classes include stocks, bonds, cash, real estate, commodities, or gold. Then, for example, stocks may be divided further into smaller buckets such as U.S. Stocks, International Stocks, Large Cap Stocks, Mid Cap Stocks, Small Cap Stocks, Value and Growth Stocks. By including these different asset classes, the probability is higher that some investments can provide satisfactory returns even if others are flat or losing value. Saying it another way, this may reduce the risk of major losses which can result from over-investing in a single asset class, however resilient you might predict a particular class to be.

With that said, here’s how we do it. We have created six asset allocations and over 95% of our clients are in one of three primary allocations below. In addition, we provide three others, a dividend, custom conservative, and aggressive strategy. We utilize mutual funds and exchange-traded funds as part of our in all of allocations.

Based on history and down market cycles (bear markets), that tend to coincide with recessions as you can see in the diagram below, we take offensive and defensive positions in our allocations. Our focus is to try and protect your wealth because, most importantly, once your distributions begin, a large loss just before or right after retirement could permanently damage the portfolio.

PILLAR 3: INSURANCE PLANNING

By now you’re used to paying for many types of insurance such as auto, home, life and medical. Insurance is simply a way to mitigate risk. Insurance allows you to protect yourself against potential loss and financial hardship at an affordable rate because the risk can be spread among a large group of people.

Our goal is to make sure you and your assets are protected in your current situation and for your future. Our advisors are licensed insurance agents and can work with many companies to help recommend the best solutions such as life insurance, annuities, long-term care or business continuation solutions.

PILLAR 4: TAX PLANNING

We help bridge the gap between financial advising and tax advice and hopefully by now we’ve had a chance to get to know your goals and financial big picture. Even though an accountant is the final authority on your taxes, we work side-by-side with them and you to put a long-term plan together for you.

Tax planning while working and accumulating assets is different from the retirement and distribution phase. While you work, tax strategy comes down to taking advantage of deductions, writing off expenses, and paying into tax deferred savings plans like 401(k)s, 403(b)s and health savings accounts. Paying too many taxes during this time can get in the way of accumulating wealth. Thoughtful tax planning measures allow you to defer or take advantage of beneficial tax law provisions and tax credits and make use of all applicable breaks available under the Internal Revenue Code.

During retirement you start drawing income from your assets. This can be in the form of Required Minimum Distributions (RMDs) from your tax-deferred accounts (IRAs). The IRAs are taxed at ordinary income on the entire amount withdrawn whereby only the gains are taxed on money withdrawn from after-tax investment accounts.

There are hundreds of different strategies that can be used to help you get the most benefit from tax-deferred accounts and mistakes can cost money. It’s important to work with a financial advisor with experience and proficiency in tax planning.

PILLAR 5: ESTATE PLANNING

This pillar may be last but definitely not the least. Estate planning is deciding how you want your assets to be distributed after you pass or if you are no longer able to make your own financial or health decisions. We work closely with Greenville estate attorneys, introduce them to our clients and coordinate and attend meetings with them. Prior to a meeting we perform an estate planning review with our clients to discuss basic estate planning principles and how they want their assets to be distributed. We also create a spreadsheet for the attorney which divides up the assets by probate and non-probate.

Probate assets are those that go through your Will – examples are accounts titled as Joint Tenants in Common or in one name only at a bank or investment firm, title of a house or car, and accounts that has beneficiaries listed as “My Estate.”

Non-Probate assets are those that get transferred directly to a named beneficiary and do not go through a Will – examples include a 401(k), 403(b), pension, accounts titled as Joint with Right of Survivorship, and life insurance policies.

A good estate plan should contain the following three documents and we recommend all of them:

- Last Will and Testament – decides how probate assets will be distributed after death

- Durable Power of Attorney – document that authorizes someone to act on your behalf in legal, business and financial matters for you even if you become incapacitated.

- Healthcare Power of Attorney (in South Carolina the Living Will is included within this document) – document that authorizes someone to act on your behalf to make decisions about your medical care if you cannot or are incapacitated.

The last document, may not be for everyone, but can be a good option, is a Trust. Trusts allow you to put legal conditions on how certain assets that will be distributed and can also be important for tax strategy.

Even if you aren’t a client, if you find you’re reading this and you don’t have your documents done, we urge you to consider taking the next step and completing your documents with an estate attorney.

Whether you’re just starting out on your financial planning journey or are an experienced investor, Financial Planning as a whole helps you see the big picture and set short-term and long-term goals. With our help, and incorporating the 5 Pillars of Financial Planning, you have the ability to map out your financial future, invest for the future, mitigate risk for the future, accumulate savings for the future and prepare your assets for the next generation.